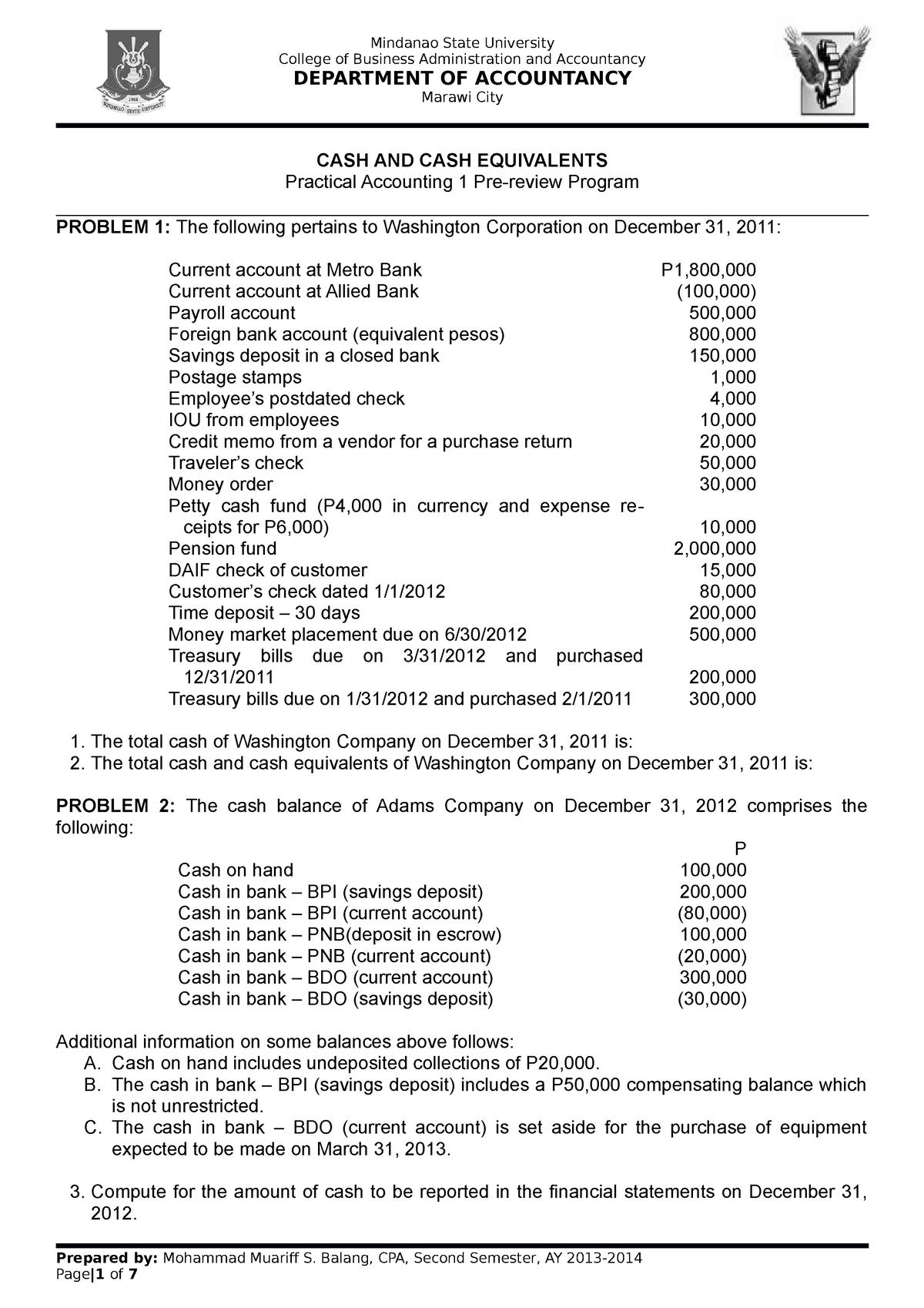

Profile dos signifies brief-title amendment results for finance changed over the expereince of living away from such amendment programs

The condition of this new cost savings around out-of modification and you will the main cause of your promoting adversity highly influence liquidation effects round the the brand new modification software. HAMP improvement took place ranging from 2009 and 2016 when you are Important/Sleek improvement taken place away from 2013 to 2017. Desk step 1 shows that forty per cent of the HAMP variations in the it try occurred in 2010 and was indeed almost certainly driven by higher financial crisis. HAMP adjustment this year remain in your state of bad guarantee an average of one year once modification.iv? The presence of bad equity greatly restricts this new borrower’s power to sell the house. Meanwhile, best quantity of Basic/Smooth adjustment took place 2014 and you may statement mediocre positive domestic equity from 21 %. The existence of self-confident household guarantee permits consumers up against financial hardships to offer their homes when you’re borrowers which have negative home collateral do not repay the borrowed funds with the arises from our home business.

Having said that, prepayment is not necessarily the dominant liquidation benefit having HAMP funds while the found to the right front side in Contour 2

It is advantageous to consider the liquidation offers to have one year off modifications in order to focus on brand new determine of your economy to your the fresh new modification lead. The year 2013 ‘s the first period both programs is actually likewise offered while the MTM LTVs one year immediately after modification was equivalent. Profile step 3 screens the liquidation offers round the both programs to possess finance changed from inside the 2013. Despite the apparently high repurchase show pursuing the HAMP amendment within the Figure step 3, prepayment (property sales) is one of repeated liquidation benefit round the one another apps. Inside first year immediately following modification both programs screen an equivalent display (up to 30 %) away from liquidation by sometimes REO otherwise foreclosure choice. While the programs’ words differed, liquidation effects is analogous for fund changed during the 2013. The condition of the brand new savings is an important consider new popularity of amendment programs.

That it blogpost simply considers the quintessential basic things towards the expertise short-title loans in Johnstown post-amendment longevity and you may liquidation shares. Comparing amendment programs’ abilities is actually a difficult task as the for every system have to be experienced relating to the current benefit. New Organizations together with Government Housing Money Company (FHFA) continuously look at several items into maintaining amendment applications or other losses mitigation solutions so you’re able to individuals against financial difficulties.

we Consumers which feel a temporary adversity and so are unable to make scheduled percentage are listed in forbearance for step 3 to 6 months. COVID-19 Forbearance and Crisis Forbearance are not loan changes.

iii An initial selling occurs when a debtor sells the home for less than the balance kept on mortgage. A deed-in-lieu is when a borrower voluntarily transmits control of the house toward proprietor of your own home loan in exchange for a production about mortgage loan and you can repayments. Financing profit happens when new People offer the fresh new changed loan to help you an exclusive investor. Prepayment refers to when the home is often offered or refinanced. REO makes reference to whenever a business gets the household inturn for terminating the mortgage after the latest foreclosure processes. A provider or servicer repurchase is when the latest Organizations need repurchase because of the solution of representations and you may guarantees.

iv Bad collateral is when new outstanding dominating harmony of the loan try higher than the market value of our home. If the financing-to-really worth ratio is more than that, the loan is considered to own negative equity.

Tagged: FHFA Statistics Blog; GSE; Fannie mae; Freddie Mac; Authorities Backed Organizations (GSEs); Household Affordable Amendment Program (HAMP); Family Maintenance Alternatives; Loan Changes

As the revealed to the left side of Figure dos, 75 % of liquidated funds concluded inside the prepayment getting Practical/Streamlined changed finance from inside the first 12 months. The new next day following amendment means the newest height on express from prepayment liquidations on 93 percent. Slowly brand new share regarding prepayments minimizes to help you 66 % regarding liquidations by 12th month. The newest reduction in the newest prepayment share are due to grows within the REO and you may foreclose choice liquidations. Within the first 12 months immediately after a good HAMP modification, 53 percent off liquidations triggered the increased loss of homeownership – 34 percent by REO and 19 per cent by the a property foreclosure solution. Ergo, the two modification software has actually seemingly equivalent durability consequences, however, slightly other liquidation pathways.