Consumers also can influence their overall incorporate rate with the addition of upwards the fresh new balances separating for the most of the handmade cards and you can breaking up of the contribution of the using restrictions.

Rating a guaranteed bank card: providing a protected bank card can help improve your FICO rating, though you aren’t eligible for old-fashioned credit cards

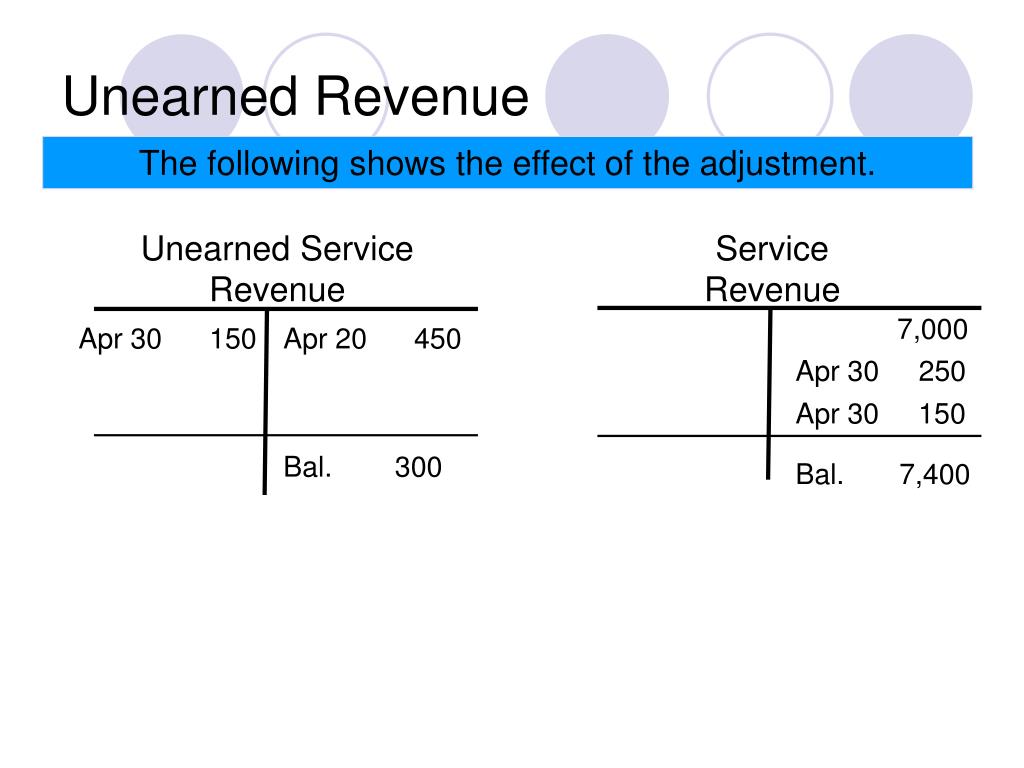

With regards to the positives, application costs more than 30 % on every account will most likely lower your credit history. As speed grows, they is likely to damage their rating a lot more.

Rates of interest was high due to the Government Reserve’s constant strive facing inflation. Whenever you are that is nice for savings profile, it is far from brilliant if you would like borrow cash.

Actually, an average credit card rate today is over 21%. Luckily for us, not absolutely all financial products have pricing that high. Home collateral financing and you will family security credit lines (HELOCs) , for example, bring pricing which might be reduced on average – generally speaking anywhere between eight and you may 10%.

For individuals who individual property, these types of domestic collateral affairs might be smart how to get brand new dollars you would like instead of accumulating heavens-high attention will cost you. But if you’re interested in delivering one to out this current year, be sure to prevent this type of five problems before you apply.

Do not sign up for almost every other credit

Never make an application for a different credit card or financing while looking to get a house security loan otherwise HELOC in the future. For starters, this can lead to a painful borrowing from the bank query.

“Borrowing inquiries down credit scores,” claims Rebecca Franco, a monetary therapist on Family unit members Trust Credit Commitment. “A lowered credit history could up coming affect the rate you be considered to possess and risk your chances of acceptance from the progressing the debt-to-earnings ratio.”

Your debt-to-money ratio (DTI) is where the majority of your monthly income the debt payments bring up. Having domestic collateral finance and you will HELOCs, you’ll be able to usually you would like a beneficial DTI off 43% otherwise straight down. For people who unlock a new account or take on even more financial obligation, it might place your DTI previous it endurance.

Just after obtaining losses minimization, you could potentially qualify for that loan amendment to help make the repayments more affordable. If you are happy to move on, you can avoid a foreclosures from the attempting to sell the house to own enough to settle the mortgage or finishing a primary marketing (with the lender’s permission).

Or you could manage to supply the property online payday loan Kentucky to your financial within the a deed unlike foreclosurepleting any of these or any other losses minimization alternative will minimize brand new preforeclosure techniques.

Plus, when you look at the preforeclosure months, most people score a limited length of time-possibly under state legislation or even the mortgage contract’s terminology-to reinstate the borrowed funds (spend the money for overdue repayments plus fees and you may can cost you). Reinstating the borrowed funds closes brand new property foreclosure techniques, and you also restart to make their normal month-to-month home loan repayments.

“Preforeclosure” in this article setting the amount of time between your financial standard and you can the new property foreclosure marketing. not, once again, many people call that time prior to a foreclosure begins the newest “preforeclosure” several months. Often, the whole techniques simply called “foreclosure.” At any rate, the borrower possess possibilities to afford the overdue amounts otherwise works out a loss of profits minimization solution in advance of a property foreclosure business happens. Continue reading “How to handle it If your Domestic Goes into Preforeclosure” »

On a great vowed so you’re able to changes our very own case of bankruptcy rules to make it more comfortable for household to help you remain in their houses

In case your credit relationship brings credit so you’re able to active obligation Provider players, their family users or dependents, you’re likely to must comply with a last signal this new Department regarding Cover (DOD) has actually provided installing the newest requirements for the majority low-home loan associated credit purchases (Last Signal). 1 The final Rule amends new regulation DOD promulgated beneath the a portion of the John Warner Federal Safety Authorization Operate for Fiscal Seasons 2007 known as Army Financing Work (MLA). dos The very last Signal increases coverage of most recent regulation to include of many low-financial associated credit deals included in possible in Credit Act (TILA), step 3 once the used from the Regulation Z. 4 It gives safer harbor tips for pinpointing consumers protected by the very last Signal, prohibits the aid of specific methods, and you may amends the message of needed disclosures. Continue reading “Complying with Previous Changes to the Army Lending Operate Controls” »

If you would like explore a great Va loan to have second household, there are several situations just be sure to believe. To be honest, there are more than just a number of affairs. With the and additionally front, you’ll be able to get the next home with a beneficial Virtual assistant financing make sure. On the without side, it isn’t due to the fact straightforward as you might promise. That’s because the brand new Virtual assistant loan system is created mostly for just one thing: to simply help active armed forces services players and you will veterans afford a home. And it is extremely, very good at that one of the best regulators programs for housing. If you prefer they to complete a couple of things, instance to buy multiple domiciles, its quicker clear. Which is Okay or even mind performing a little research (steer clear of the).

While you are mindful, you can get a couple belongings using your Va masters. It isn’t illegal, you must recognize and stick to brand new VA’s policies. Meaning insights regulations from the occupancy, entitlement, and you can eligibility. And also have good calculator ready as you could need to do particular mathematics.

Time was Everything you: Occupancy Requirement

Occupancy ‘s the first difficulty. Brand new You.S. Institution from Pros Circumstances requires that after you apply for a beneficial Virtual assistant mortgage be sure, it should be into the house in fact it is much of your domestic. With regards to timing, to acquire the next assets having a beneficial Virtual assistant loan extremely means you are to shop for a primary quarters, leaving your own earlier in the day household since your second domestic. Continue reading “Having fun with an excellent Virtual assistant Mortgage to have Next Household | Cut having Land getting Heroes” »

Contain which Family Depot Mastercard on wallet without any additional annual will cost you, because does not charges a yearly payment.

One year and come up with yields

Once you shell out on Household Depot Mastercard, you really have 365 months from the big date from pick to get an entire refund, which is lengthier as compared to practical 90 days Your house Depot generally also provides. And if you’re shed your own bill, The house Depot can to obtain it in program.

Good for strengthening borrowing from the bank

Among pressures of increasing your credit rating is seeking a https://paydayloansconnecticut.com/derby/ credit your qualify for. Of a lot want a high credit history, and people who cannot normally have a myriad of a lot of charges.

Every train journey to and from work would always see me with my latest' horror find' perched in my lap, trying to finish just that one more page before.